If you’re considering a sale of your business in 2026 or beyond, here’s a snapshot of the current M&A landscape and recent valuation trends:

Big Picture — Valuations are strong and climbed in the third quarter, even as year-to-date deal volume is below last year’s pace.

We expect a solid start to M&A in 2026, assuming equity markets remain stable and there’s no broader economic slowdown.

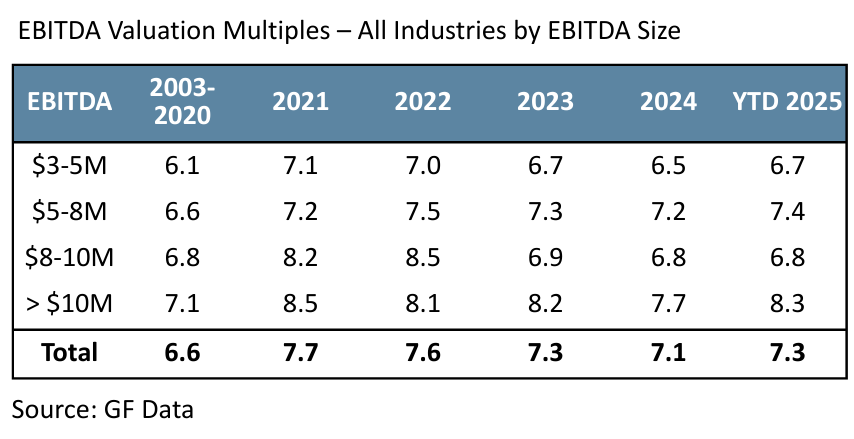

Average purchase price multiples grew to 7.3x TTM EBITDA in Q3, up from 6.9x in Q2. While not at post-COVID levels, valuations are healthy, compared to historical averages.

Private equity firms are paying more for add-on acquisitions that complement existing portfolio companies. For all deals below $25 million in EBITDA, add-on acquisitions by PE firms averaged 6.9x TTM EBITDA valuation this year, compared to 5.9x TTM EBITDA for platform acquisitions.

Deal volume dropped. The number of deals closed year-to-date is down by 25% compared to the same period last year, reflecting hesitancy from sellers to start the exit process earlier this year. Financially strong businesses (with above average financial metrics) also dropped to 44% of businesses sold, down from historical norms of 55%.

Historically, lower deal volume pressures valuations. Today buyers are instead paying more for the stronger businesses that are available.

Tariffs are still negatively impacting M&A activity, but with some nuance. Buyers in industries reliant on imports hit pause on M&A earlier this year, while they dealt with their own tariff challenges. Some of these buyers are now looking for acquisitions to drive growth.

On the seller side, companies with high gross margins, supply chain flexibility, or the ability to quickly pass along price increases with no drop in customer demand are in better shape to consider an exit than importers of lower cost, non-branded, or commodity products.

Overall, increased buyer interest, strong valuations and potential future interest rate cuts bode well for entrepreneurs considering an exit, with the usual caveat that any decline in the US equity markets will also create a slowdown in M&A activity.

That said, the most important driver of M&A success is always the recent performance and future potential of your individual business. In this environment, if your business is healthy, you can expect a positive reception from a range of buyers.

Sources: GF Data, S&P, Pitchbook, NRF.

About Hughes Klaiber

Hughes Klaiber is an investment banking firm specializing in lower middle market companies. We help business owners maximize value and navigate successful exits to private equity and strategic buyers. Our team brings deep experience, hands-on execution, and trusted guidance throughout the transaction process. Schedule a confidential call here or learn more at www.hughesklaiber.com.

646-654-0458

info@hughesklaiber.com

1185 Avenue of the Americas

Third Floor

New York, NY 10036